基于GARCH模型股票组合投资策略应用研究

首发时间:2019-06-10

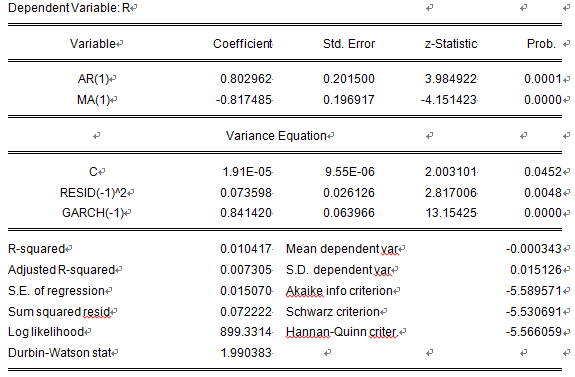

摘要:本文为了确定股票最优组合投资策略,综合考虑股票投资的收益和风险,建立以投资收益最大化和风险最小化为目标的双目标优化模型,并引入乐观系数将双目标转化为单目标。本文以中国石油、中国石化、中国银行和中国工商银行为目标股票进行最优组合投资策略的确定。基于GARCH模型确定四支目标股票的平均收益率和风险损失率,将其代入优化模型,得到最优的投资组合策略。

For information in English, please click here

Research on Application of Stock Portfolio Investment Strategy Based on GARCH Model

Abstract:In order to determine the optimal portfolio investment strategy, considering the return and risk of stock investment comprehensively, this paper establishes a two-objective optimization model aiming at maximizing the return of investment and minimizing the risk, and introduces optimism coefficient to transform the two objectives into a single objective. This paper takes PetroChina, Sinopec, Bank of China and Industrial and Commercial Bank of China as the target stocks to determine the optimal portfolio investment strategy. The average return rate and risk loss rate of four target stocks are determined based on GARCH model. The optimal portfolio strategy is obtained by substituting them into the optimization model.

Keywords: GARCH Model Portfolio Investment Optimism Coefficient

基金:

论文图表:

引用

No.****

动态公开评议

共计0人参与

勘误表

基于GARCH模型股票组合投资策略应用研究

中国科技论文在线 版权所有

网站地图|

在线首页|

在线简介|

服务条款|

联系我们

京公网安备 11040202430024号 京ICP备15006316号-2| 网络出版服务许可证 (总)网出证(京)字第083号 | 文保网安备案号:1101080066

.txt

.txt .ris

.ris .doc

.doc

评论

全部评论