жӮЁеҪ“еүҚжүҖеңЁдҪҚзҪ®пјҡ

йҰ–йЎө > йҰ–еҸ‘и®әж–Ү

0

0

жҜ”зү№еёҒжңҹиҙ§жҺЁеҮәеҜ№зҺ°иҙ§еёӮеңәжіўеҠЁзҡ„еҪұе“Қз ”з©¶

йҰ–еҸ‘ж—¶й—ҙпјҡ2020-06-11

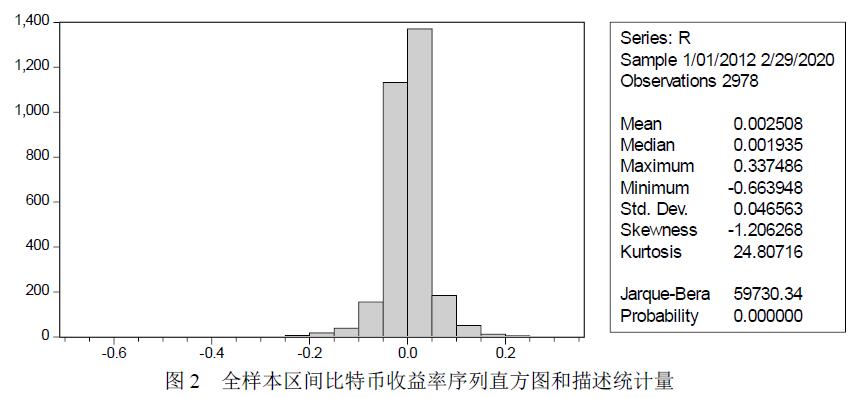

ж‘ҳиҰҒпјҡиҠқеҠ е“ҘжңҹжқғдәӨжҳ“жүҖпјҲCBOEпјүе’ҢиҠқеҠ е“Ҙе•Ҷе“ҒдәӨжҳ“жүҖпјҲCMEпјүе…ҲеҗҺдәҺ2017е№ҙ12жңҲ10ж—ҘпјҢ12жңҲ18ж—ҘдёҠзәҝжҜ”зү№еёҒжңҹиҙ§пјҢзӣ®еүҚеҜ№дәҺдё»жөҒйҮ‘иһҚжңәжһ„жүҖжҳҜеҗҰеә”иҜҘжҺҘзәіжҜ”зү№еёҒиҝҷзұ»й«ҳйЈҺйҷ©иө„дә§иҝҳеӯҳеңЁе№ҝжіӣдәүи®®гҖӮжң¬ж–ҮеҹәдәҺGARCHж—ҸжЁЎеһӢеҲҶжһҗжҜ”зү№еёҒжңҹиҙ§зҡ„жҺЁеҮәеҜ№зҺ°иҙ§еёӮеңәжіўеҠЁзҡ„еҪұе“ҚгҖӮе®һиҜҒз»“жһңжҳҫзӨәпјҢжңҹиҙ§жҺЁеҮәеҗҺпјҢзҺ°иҙ§еёӮеңәжіўеҠЁеўһеӨ§пјҢдё”жіўеҠЁзҡ„еўһеҠ 并йқһжҳҜз”ұдәҺдҝЎжҒҜдј йҖ’йҖҹеәҰеҠ еҝ«йҖ жҲҗзҡ„пјҢиЎЁжҳҺжҜ”зү№еёҒжңҹиҙ§дәӨжҳ“зҡ„дёҠзәҝзЎ®е®һеҠ еү§дәҶзҺ°иҙ§еёӮеңәзҡ„дёҚзЁіе®ҡжҖ§гҖӮжҜ”зү№еёҒзҺ°иҙ§еёӮеңәеӯҳеңЁзқҖйқһеҜ№з§°ж•Ҳеә”пјҢжңҹиҙ§жҺЁеҮәеҗҺпјҢйқһеҜ№з§°ж•Ҳеә”еўһејәгҖӮж №жҚ®е®һиҜҒз»“и®әпјҢжң¬ж–ҮжҸҗеҮәеҠ ејәзӣ‘з®ЎеҠӣеәҰгҖҒдё°еҜҢжңҹиҙ§дә§е“ҒгҖҒеҠ ејәжҠ•иө„иҖ…ж•ҷиӮІзҡ„е»әи®®гҖӮ

е…ій”®иҜҚпјҡ дә’иҒ”зҪ‘йҮ‘иһҚ жҜ”зү№еёҒжңҹиҙ§ GARCHжЁЎеһӢ жіўеҠЁжҖ§

For information in English, please click here

Research On The Impact Of Bitcoin Futures On Spot Market Volatility

AbstractпјҡChicago Board Options Exchange (CBOE) and Chicago Mercantile Exchange (CME) launched Bitcoin futures on December 10 and December 18, 2017.This marked the formal acceptance of bitcoin derivatives by mainstream financial institutions. At present, there is a debate on whether the official institutions should accept high-risk assets such as bitcoin.Based on GARCH model, this paper analyzes the impact of bitcoin futures on spot market volatility.The empirical results show that after the introduction of futures, the fluctuation of spot market increases, and the increase of fluctuation is not caused by the acceleration of information flow speed. It shows that bitcoin futures trading aggravates the instability of the spot market. There is an asymmetric effect in the bitcoin spot market. After the introduction of futures, the asymmetric effect increases. According to the empirical conclusion, this paper puts forward three suggestions: strengthen supervision, enrich futures products, and strengthen investor education.

Keywordsпјҡ Internet finance Bitcoin futures GARCH model Volatility

еҹәйҮ‘пјҡ

и®әж–ҮеӣҫиЎЁпјҡ

еј•з”Ё

No.****

еҠЁжҖҒе…¬ејҖиҜ„и®®

е…ұи®Ў0дәәеҸӮдёҺ

еӢҳиҜҜиЎЁ

жҜ”зү№еёҒжңҹиҙ§жҺЁеҮәеҜ№зҺ°иҙ§еёӮеңәжіўеҠЁзҡ„еҪұе“Қз ”з©¶

дёӯеӣҪ科жҠҖи®әж–ҮеңЁзәҝ зүҲжқғжүҖжңү

зҪ‘з«ҷең°еӣҫ|

еңЁзәҝйҰ–йЎө|

еңЁзәҝз®Җд»Ӣ|

жңҚеҠЎжқЎж¬ҫ|

иҒ”зі»жҲ‘们

дә¬е…¬зҪ‘е®үеӨҮ 11040202430024еҸ· дә¬ICPеӨҮ15006316еҸ·-2| зҪ‘з»ңеҮәзүҲжңҚеҠЎи®ёеҸҜиҜҒ пјҲжҖ»пјүзҪ‘еҮәиҜҒпјҲдә¬пјүеӯ—第083еҸ· | ж–ҮдҝқзҪ‘е®үеӨҮжЎҲеҸ·пјҡ1101080066

.txt

.txt .ris

.ris .doc

.doc

иҜ„и®ә

е…ЁйғЁиҜ„и®ә